Soon, all the work of the accountant shall be replaced by computers and smart algorithms. The assembly work disappears, tax advices are programmed and controls are performed automatically; the accountant only has to follow the (digital) signals. At least, these are the stories you hear everywhere around you and you may believe, following the discussion in the accountancy world. However, accountants who delve into the wonderful world of IT also see all sorts of new possibilities and opportunities arise. The combination of knowledge of accounting on the one hand and knowledge of IT on the other hand is priceless.

SMEs (small and medium-sized enterprises) heavily invest in IT, the ‘paper organization’ is shifting more and more towards a digital world. One thing all companies have in common is their increasing dependence on IT. Entrepreneurs are usually very proud of their IT solutions and like to see the accountant making use of it. If you magically come up with a number of notable transactions thanks to smart data analyses, the customer is often deeply impressed. Moreover, if these analyses for example trace double payments, you may save money for the company and further increase your added value as an accountant.

SMEs have many questions and needs in the field of IT. The exchange of data between different software packages both inside and outside the company for example. Also, the optimization of the business processes that make use of the IT systems is often high on the priority list of the Board. The SME entrepreneur can of course hire an IT company to get these matters implemented. However, the accounting firm can also fulfil an important role. The accountant has a clear advantage compared to the (equally expensive) IT expert. The accountant knows the customer well and knows all about process control and process optimization. He can better and faster foster translation of the processes through (internal) management to a good functional application in the end.

In practice, it often turns out not to be that easy to actually get started with the IT systems and the data stored therein. Major challenges the accountant has to deal with include for example:

– Outsourcing of IT;

– Improper regulation of the (primary) registration, so that data integrity is not guaranteed;

– Wide variety of packages used.

These challenges will be explained below.

Outsourcing of IT

Companies make different choices about how they organise IT. Larger companies often have an internal IT department, while SMEs more often purchase IT services externally, which will often be accessed from the cloud. This will bring important benefits to SMEs, like:

– The company does not need to maintain the hardware and software and does not require IT expertise;

– The use of new software does not require a (large) investment; the services are often billed on a monthly subscription basis;

– The service can easily be adapted to the needs of the users (scalable)

Outsourcing of IT also has certain risks.

The (technical) IT knowledge is often concentrated in the hands of a few and even outside the organization. The continuity of the IT can quickly get into danger by the loss of a single person or by a disturbed relationship with a supplier.

Another major challenge is the shared responsibility of the IT infrastructure. Internally, one is responsible for the functional part of the applications while the system is invested externally. Who is responsible for matters like the proper functioning of the backups, database management, information security, or extremely slow systems? This often requires a joint effort, about which sound agreements must be made.

The auditor can play an important role in the communication between the company and the external IT service provider, for example in making proper arrangements and the recording thereof in a Service Level Agreement. The auditor can also be pivotal in the translation of the needs of the customer into the technical implications of it.

Data integrity

Data integrity refers to the accuracy, completeness and timeliness of the data. This applies to the input of data, the processing of these data by the system and the output of the system (for example reports). In order to ensure data integrity, recording data definitions is an important first step. Defining the concepts and terms used in an organization may seem to be a simple task at first glance, but in practice there appear to be interpretation differences surprisingly often. Clarity on issues such as the method of calculation and any filters or aggregates prevents much confusion.

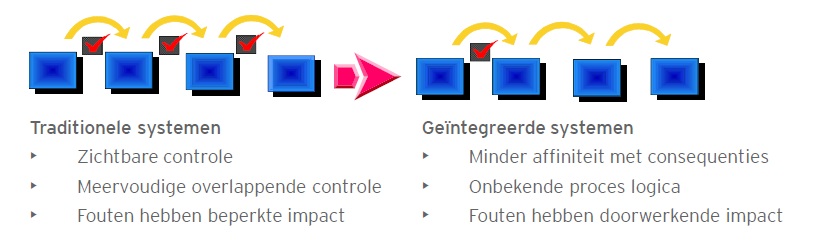

Automation should force a large part of the data integrity. However, control remains essential because the system cannot take into account all exceptions. More people watched the transactions in traditional systems. Multiple eyes could detect errors. In embedded systems, the system performs many checks ‘in the background’ which are less visible to users. An error in a programmed control can therefore lead to a structural error with a big impact. In Figure 1 a few key differences between traditional systems and integrated systems are displayed.

Figure 1. Integrated IT systems versus traditional systems

The reliability of data depends to a large extent on the people who use the IT systems. However good the IT systems are when tested in advance, they will never be able to give a 100% guarantee. The responsibility for the reliability of the information should be embedded in daily operations as well. The expertise of the auditor comes in very handy here.

Wide variety of packages

Each system has its own characteristics and hence its own specific risks. Even ‘standard’ systems contain a lot of company-specific settings. Especially with the more complex packages it is therefore hardly possible to make a distinction between standard and custom software.

Despite many differences, the auditor may still be of great value in the implementation or optimization of an IT system. Regardless of the system used a company should always consider to implement an authorization model, a process flow and controls; all of these subjects integrate seamlessly with the knowledge and skills of the modern accountant.

Future of the accountant

The modern digital world offers many new opportunities. Just think of the possibilities of analyzing, interpreting, visualizing and monitoring the integrity of all data streams that are in a company, flow through the company and in the end leave the company.

A major challenge for the current generation of accountants is overcoming the large knowledge gap in the field of IT. IT is not (yet) in the broad field of accountancy. Only an IT-mindset and a good will are not enough to simply pick up. One way to reduce this backlog is to employ IT experts who are able to implement the technical component.

In addition to this, the accountant will also need different and probably more knowledge of the customer than what is now collected through an average (assembly) task. Without understanding the (daily) business processes of the client, it is almost impossible to sufficiently distinguish the different data streams and use them.

The accountant will have to invest in IT in the coming years, but will definitely face a successful future!