The first part of this two-part article introduced the possibilities a government has to implement countercyclical policies: making use of automatic stabilizers and discretionary fiscal policy. This last part analyses the effects of the recent recessions on the development of the four components1 of the Dutch GDP. I conclude with a policy advice to the next government.

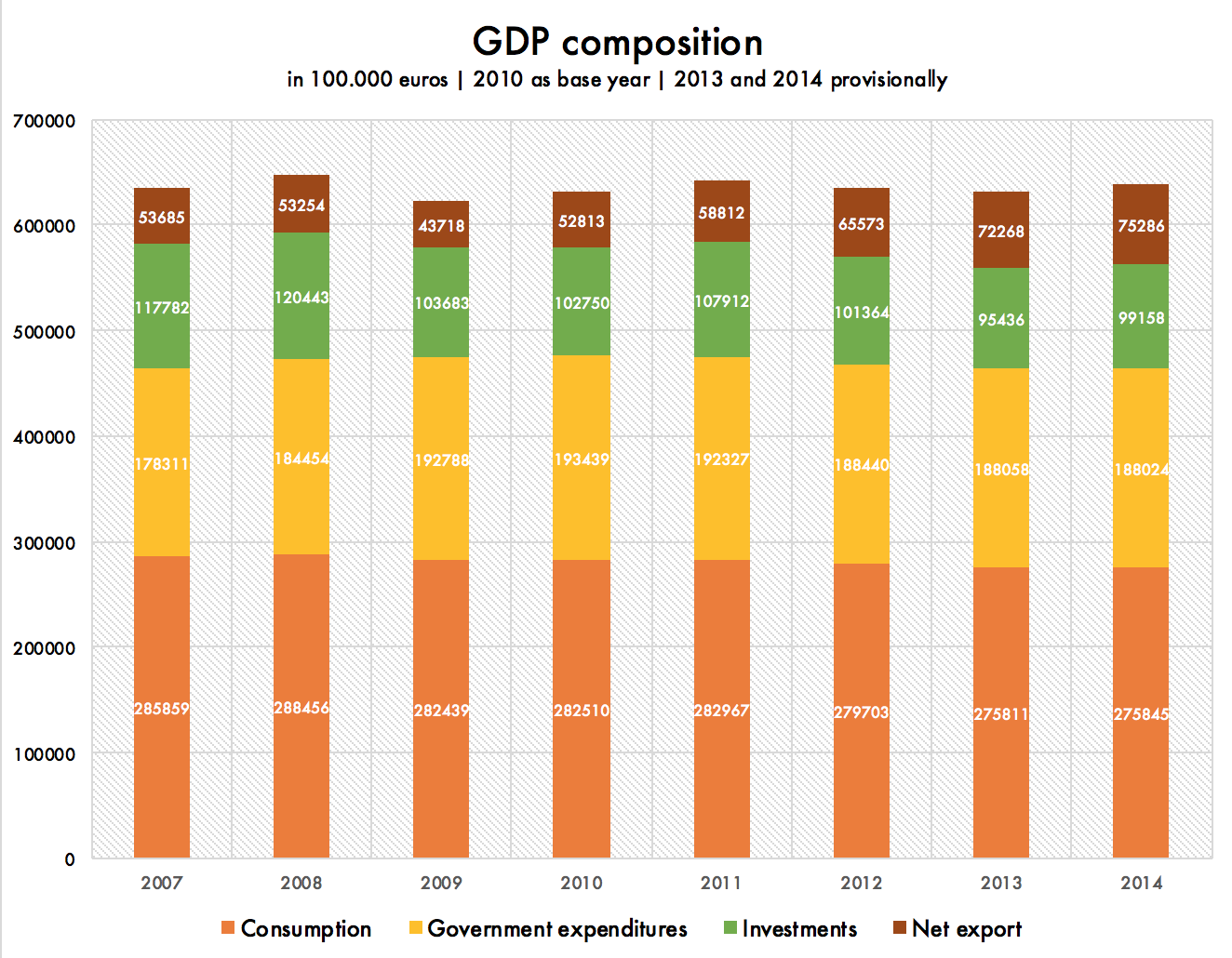

Dutch households have got the highest mortgage debt of the Eurozone (€ 638 billion). As the virtual value of real estate seemed to rise by default, taking up (mortgage) loans was relatively easy prior to the crisis. People found themselves richer than they actually were, which resulted in excessive consumption. When the truth about real estate valuations eventually revealed itself, consumption expenditures needed to be cut. The Dutch consumption expenditures dropped by as much as 3.5% over the period 2007-20142, while GDP had a similar size in both periods (see graph).

Furthermore, one may also observe a sharp drop in investments. As of difficult market conditions (less confidence and falling demand) companies went bankrupt and investments had been eliminated. Companies that were able to survive the crises scaled back their investments drastically. A corresponding result can be observed in the data: investments fell by as much as 15.8% over the years 2007 to 2014. Next to consumer spending, investments are still far from full recovery.

Despite a decline of 18.6% in the 2007-2009 period, net exports (NX) have returned to their previous levels as early as 2011. At first, confidence in international trade declined, but this proved short-lived and net exports recovered rather quickly. Indeed, in 2014 net exports had increased by 40% compared to 2007. The exporting sector is often the first sector that kick-starts after an economic downturn. This is certainly applicable to the Netherlands as it is a small and open economy.

Finally, government spending has not declined but increased at a slower pace than would have been the case without government intervention. In total, government expenditures increased by 5.4% over the years 2007 – 2014. Despite the implementation of some austerity measures, absolute government spending increased yearly. The budget cuts were primarily intended to counteract the effect of automatic stabilizers, which resulted in government spending increasing less quickly.

‘’… GDP could have been higher in 2014 if the government did not cut its budget and made use of expansionary fiscal policy.’’

In the end, especially thanks to an increase in exports, GDP recovered in seven years. Consumption and investment dropped significantly. Despite the fact that government spending showed a small increase, the government has made every effort to prevent this from happening. Its goal was to oppose the effects of the automatic stabilizers, leading to a prolonged recession. In other words, GDP could have been higher in 2014 if the government did not cut its budget and made use of expansionary fiscal policy. During a recession the government should implement countercyclical policies instead of procyclical ones. This will weaken the business cycle, lead to less volatility and mitigate the adverse effects of the downturn.

Well, you could argue that the Dutch government did not have the means to implement expansionary policies during the recession. That’s totally correct. The Stability and Growth Pact (3% rule) obliged the cabinets Rutte I and II to deepen the recent recessions. As the government did not succeed in cutting the budget sufficiently in the years preceding the crises (when a boom was going on) and did not refrain from using expansionary fiscal policy, it had been implementing procyclical fiscal policy in an economic upturn. The government actually increased volatility.

‘’ The government will need to run a budget surplus (towards + 3%) to make countercyclical fiscal policies feasible in the event of a new recession.’’

To mitigate the effects of a new recession the government will have to go back to austerity measures once again. The government will need to run a budget surplus (towards + 3%) to make countercyclical fiscal policies feasible in the event of a new recession. The government will have to repair its roof right now because if we take a look outside, it stopped raining and the sun has returned. You will never know when it starts raining again…

1 Consumption (C), investments (I), net exports (NX) and government expenditures (G).

2 I have chosen the 2007 – 2014 period as the economy was almost equally large in terms of GDP in both years. This enables us to observe changes in the composition of the GDP.

Max Pepels is a blogger at econooMax. Do you want to read more of Max? Visit the website of econooMax!